Texas has always done things at scale. But nothing in ERCOT’s history has tested the grid quite like the current wave of large load growth. In less than four years, the Lone Star State has become the epicenter of a global race to build AI data centers, hyperscale cloud campuses, semiconductor fabs, battery gigafactories, and LNG export infrastructure — all demanding power at a speed and scale that the grid was simply not designed to absorb.

Large load interconnection queue as of April 22, 2026

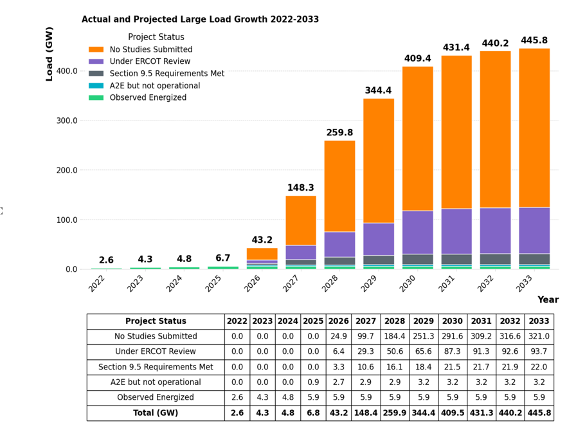

ERCOT’s interconnection queue, once a manageable pipeline of loads, has been transformed into a bottleneck for large electricity consumers. As of mid-2026, the grid operator is managing requests representing 445GWs of prospective new load by 2033 — a number that would have been unimaginable a decade ago. For every project that successfully connects, dozens more are waiting in a queue measured not in months but in years.

The stakes are high. Texas’s economic competitiveness, its ability to attract and retain next-generation industries, and the reliability of power for its 30 million residents all hang in the balance. How ERCOT and its stakeholders respond over the next five years will determine whether Texas leads the AI economy — or cedes that ground to other states and countries that move faster.

WHAT IS DRIVING LARGE LOAD GROWTH?

Data Centers and AI Infrastructure

The single largest driver of new large load in ERCOT is data center development, and within that category, the buildout of AI training and inference infrastructure is the dominant force. The shift from conventional cloud workloads to GPU-dense AI clusters has fundamentally changed the power calculus for developers. A hyperscale data center that might have consumed 50–100 MW a decade ago now anchors campuses that target 500 MW to 1 GW of continuous power demand.

Texas offers a convergence of advantages that few other markets can match: abundant land, relatively streamlined permitting, a deregulated electricity market that allows creative supply arrangements, proximity to natural gas infrastructure, and a growing fiber backbone. The Dallas–Fort Worth metroplex, Austin, San Antonio, and emerging markets in West Texas have all seen significant data center activity.

Announced and under-construction data center capacity in Texas reached record levels in 2025 and 2026, with major hyperscalers, colocation providers, and dedicated AI infrastructure companies all competing for sites with viable power. The operational challenge is no longer finding land or the fiber — it is finding the electrons.

Industrial Electrification and Nearshoring

Beyond data centers, ERCOT is absorbing a second wave of large load driven by industrial electrification and the broader reshoring of manufacturing to the United States. The CHIPS Act, the Inflation Reduction Act, and shifting global supply chain strategies have accelerated investment in semiconductor fabrication, electric vehicle component manufacturing, hydrogen production, and advanced materials processing — all of which are electricity-intensive.

Several large semiconductor fabs have been announced or are under construction in the Texas Hill Country and Central Texas corridor. Electrolytic hydrogen production facilities, which require massive amounts of continuous power to split water molecules, are also being developed in West Texas to take advantage of abundant wind and solar resources.

LNG export terminal expansions along the Gulf Coast, while primarily gas infrastructure, also require significant electrical power for compression, liquefaction, and auxiliary systems — adding another layer of demand to the ERCOT South and ERCOT South-Central load zones.

Bitcoin Mining and Flexible Load

Texas remains the dominant U.S. market for Bitcoin and cryptocurrency mining, attracted by competitive electricity prices, the deregulated market structure, and a regulatory environment that has generally been accommodating. Large mining operations, which can consume hundreds of megawatts each, have a unique characteristic that distinguishes them from most industrial loads: they are highly flexible and can curtail their consumption within minutes when the grid is stressed.

This flexibility has made Bitcoin miners both a challenge and an asset for ERCOT. As large loads, they add to the integration burden during normal operations. But as interruptible resources enrolled in demand response programs, they provide a valuable reliability backstop during peak events. ERCOT has leaned heavily on this flexibility, and the relationship between the grid operator and the mining sector has evolved into a more formal demand response framework.

THE INTEGRATION CHALLENGE

The Interconnection Queue Bottleneck

The fundamental challenge of large load integration in ERCOT is not the physical capability of the grid — Texas has been building transmission aggressively for two decades — but rather the administrative, study, and construction pipeline required to connect new loads at transmission voltage.

ERCOT’s large load interconnection process requires new customers above certain thresholds to undergo a series of power flow studies, stability analyses, and — in many cases — transmission upgrades before they can receive service at their requested load level. These studies are sequential: each new applicant must wait for the studies ahead of it in the queue to be completed before its own analysis can begin. As the queue has grown exponentially, study timelines have stretched accordingly.

For a developer seeking a 500 MW data center campus with a direct transmission-level interconnection, the realistic timeline from application to full commercial power is 4–6 years under current conditions. For projects requiring new substation construction or significant transmission line upgrades, that timeline can stretch further. In a market where AI infrastructure developers are under pressure to deliver capacity in 18–24 months, this creates an acute mismatch.

Moreover, the Public Utility Commission of Texas (PUCT) is codifying a new gating framework through Project 58481, the rulemaking implementing PURA § 37.0561 as enacted by Senate Bill 6 in the 89th Legislative Session. The Proposal for Publication of 16 TAC § 25.194 — Large Load Interconnection Standards — was issued on March 12, 2026, confirming the 75 MW threshold and introducing formal “Intermediate Agreement” requirements that an applicant must satisfy to remain in the study queue. These include documented site control, posted financial security (proposed at $50,000/MW, with roughly 20% refundable upon achieving commercial operation), backup generation disclosures, and expanded transparency obligations covering corporate affiliates, end-use, and behind-the-meter generation. The intent is to filter out speculative requests that have been clogging the queue and to ensure that loads counted in transmission planning are genuinely going to be built.

Transmission Constraints and Congestion

Even where transmission capacity exists in theory, the geographic distribution of new load requests is creating pockets of severe congestion. The DFW metroplex, which has attracted the highest concentration of data center development in Texas, is served by a transmission system that was designed around the load patterns of a major metropolitan area — not the superimposition of hundreds of additional megawatts of always-on computing infrastructure.

Similar dynamics are playing out in the Austin–San Antonio corridor and in parts of West Texas where data center developers are trying to co-locate with wind and solar generation. Transmission congestion creates both reliability risks and economic distortions: when generators cannot export power to where it is needed, or when load pockets develop that cannot be fully served, the result is both higher costs and reduced reliability.

PUCT and ERCOT have responded by accelerating transmission planning in high-demand areas and by working with transmission-owning utilities — primarily ONCOR, AEP Texas, and CenterPoint — to identify and prioritize upgrades. Several major transmission projects aimed specifically at relieving data center-driven congestion have been approved and are in various stages of construction.

Reliability and Adequacy

The sheer pace of load growth creates a structural challenge for ERCOT’s resource adequacy framework. Traditional resource planning assumed relatively predictable load growth that could be met by a combination of new generation investment and demand response. The current environment — where gigawatts of new load can appear on the planning horizon in a matter of months — strains that framework significantly.

ERCOT’s Capacity, Demand, and Reserves (CDR) report has been revised upward multiple times in recent years as new large load projects materialize faster than expected. The concern is not merely that peak demand will be higher — it is that the pace of load growth may outstrip the ability of generation investment and transmission expansion to keep pace, creating a window of elevated reliability risk during the transition period.

This concern is magnified by the fact that much of the new generation being built to serve large load growth — particularly natural gas capacity developed as BTM solutions — takes time to permit, build, and commission. There is a meaningful lag between the moment a large load developer commits to a project and the moment that project’s associated generation is online and reliable.

The path forward is not obvious — but it is taking shape. In Part 2 of this series, CES unpacks the strategies that could accelerate time to power for these large loads, and the bold moves ERCOT, regulators, and developers must make to keep Texas at the front of the pack.

Navigating large load integration in ERCOT or another market? Our consulting team is ready to help, contact us to learn more about how CES can support your strategy.

By: Pranao Walker, Lead Consult, Energy Advisory