Introduction

The push for electrification often focuses on securing minerals such as lithium, nickel, cobalt, graphite, and rare-earth elements. As demand for electric vehicles, energy storage, and renewable energy grows, governments and industries are spending billions to secure these resources. Yet another key material often goes unnoticed in these discussions: sulphuric acid, which is just as important for the clean energy transition.

Recent tensions in the Middle East and problems with shipping through the Strait of Hormuz have pushed up sulphur and sulphuric acid prices. Although sulphur does not get as much attention as lithium or nickel, its use in processing battery materials means that price swings can affect the whole EV supply chain.

India is working hard to localize battery production through the ACC PLI scheme and the National Critical Minerals Mission. The growing sulphur issue shows that just securing minerals is not enough. Having access to the chemicals needed to process these minerals is just as important.

Sulphur Hidden Role in Battery Supply Chain

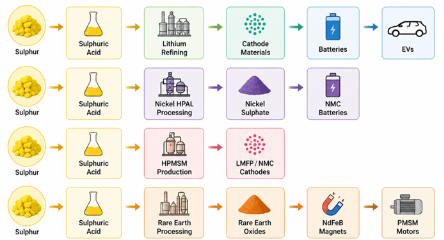

Sulphuric acid is a key chemical used to extract, leach, roast, and purify important battery minerals. It plays a central role in making lithium, processing nickel, separating rare earths, and producing manganese sulphate, making it essential to many battery supply chains.

Figure 1: Sulphur Dependency Across Battery Materials and EV Manufacturing

Source: CES Analysis and secondary sources

Battery makers usually focus on securing sufficient supplies of lithium, nickel, cobalt, and graphite. However, the price and supply of sulphuric acid can have a big impact on battery production costs. As demand for batteries rises, the industry relies even more on processes that consume large amounts of sulphur. India is highly dependent on sulphur imports, sourcing over 50% its annual requirement from Middle East countries1. Countries like UAE, Oman, and Saudi Arabia supply more than 80% of India’s sulphur requirement which goes majorly into fertilizer industry2. The Middle East accounted for around a quarter of global sulphur production at 83.87 million metric tons in 2025, according to the U.S. Geological Survey.

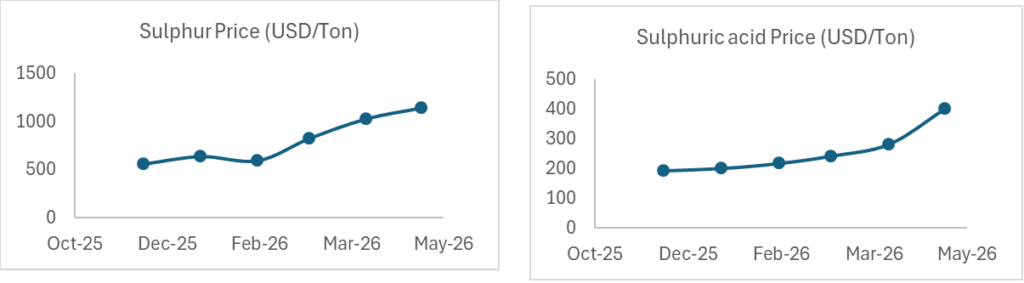

Figure 2: Sulphur and Sulphuric Acid Prices (2025-2026) (USD/Ton)

Source: Trademap

Industry sources say sulphur prices have risen by more than 100% globally, and sulphuric acid prices have more than doubled since the conflict in Iran began. What used to be a stable cost is now a major expense for battery material producers. For instance, the price of sulphur rose to US$ 1,150/ton in May 2026 from US$ 525/ton in late 2025 whereas sulphuric acid price escalated to US$ 400/ton in 2026 from $200/ton in late 20253.

Lithium Refining Under Pressure

Lithium is central to modern rechargeable batteries, but converting lithium ore into battery-grade chemicals depends heavily on sulphuric acid. Globally, about 99% of hard-rock lithium processing uses sulphuricacid roasting, making it essential for producing battery-grade lithium from spodumene and mica. A typical operation processing 200,000 tonnes of ore annually may require 30,000 to 50,000 tonnes of sulphuricacid for leaching alone, highlighting the sector’s strong dependence on sulphur-based processing.

The lithium industry is especially sensitive to higher sulphuric acid prices. Industry estimates show that the cost of acid in lithium chemical production has tripled in just six months due to increasing consumption of sulphuric acid in lithium chemical production. Sulphuric acid, once a minor expense, is now one of the most unpredictable and largest costs in lithium refining. It used to make up 3% of the cost to produce lithium chemicals from hard rock, but now it is 11% and has become the highest single cost, even more than energy4. Therefore, according to CES estimates, a sustained sulphur price shock could increase EV battery pack costs by 2-5%, with nickel-rich chemistries and batteries reliant on sulphate-based precursor production being particularly exposed.

Nickel Supply Chain Risks

Among all battery materials, nickel production through High Pressure Acid Leach (HPAL) technology is perhaps the most sulphur-intensive. HPAL facilities process laterite nickel ores using large volumes of sulphuric acid to produce Mixed Hydroxide Precipitate (MHP), which is subsequently refined into battery-grade nickel sulphate. As per industry estimates that each tonne of contained nickel produced through HPAL may require more than 10 tons of sulphur5. A rise in sulphuric acid prices from approximately US$200/t to US$400/t can increase operating costs by an estimated 25-45%, depending on acid consumption rates and ore characteristics. Since sulphuric acid is one of the largest reagent inputs in HPAL processing, higher acid prices can significantly erode margins and raise the cost of nickel units produced6.

Indonesia has emerged as the world’s largest nickel supplier through HPAL projects that produce Mixed Hydroxide Precipitate (MHP), a critical precursor for battery-grade nickel. About 76-80% of Indonesia’s sulfur is imported from the Middle East, and Indonesia’s sulfur imports surged to 5.35 million metric tons in 2025, up 48% year-over-year, driven by the rapid expansion of High-Pressure Acid Leach (HPAL) processing7. However, this critical supply line is under severe pressure due to Middle East geopolitical conflicts and the disruption of shipping through the Strait of Hormuz.

Nickel-rich cathode types like NMC (Nickel Manganese Cobalt) and NCMA are still the main choice for long-range EV batteries. India now imports most of its battery-grade nickel, but future investments in making cathode materials could face higher costs if sulphur prices stay unstable. Indian companies that buy nickel intermediates from Indonesia may end up paying more because of these increased production costs.

HPMSM: The Overlooked Battery Material Facing Sulphur Risk

Lithium and nickel usually get most of the attention in battery supply chain talks, but High Purity Manganese Sulphate Monohydrate (HPMSM) is also becoming important and is affected by changes in sulphuricacid prices. HPMSM is a key ingredient for high-manganese cathodes and NMC battery types that are being used more in electric vehicles.

The production of battery-grade manganese sulphate is highly dependent on sulphuric acid. Manganese ores are leached and purified using large amounts of acid before they become HPMSM. So, if sulphuric acid prices stay high, the cost to produce HPMSM also goes up. Battery manufacturers are exploring manganese-based cathode materials as a cost-effective alternative to nickel-rich chemistries. India’s ambition to localize cathode active material (CAM) production under the Advanced Chemistry Cell (ACC) PLI scheme could face higher input costs if sulphuric acid markets remain volatile. As demand for lithium iron phosphate (LFP), LMFP, and manganese-rich NMC batteries expands, securing stable sulphuric acid supplies will become increasingly important for maintaining competitiveness in domestic cathode manufacturing.

Copper Foil Manufacturing Faces Upstream Risks

Copper is also a key part of batteries. Every lithium-ion battery uses copper current collectors, and electric vehicles need a lot of copper for wiring, busbars, charging stations, and power electronics. Over 20% of the world’s mined copper is made using solvent extraction-electrowinning (SX-EW), which requires approximately 2-3 tonnes of sulphuric acid per tonne of copper cathode produced, with consumption rising above 5 tonnes per tonne of copper for highly acid-consuming ore 8. So, higher sulphur costs can affect how much it costs to produce copper and its price further down the supply chain.

This issue is becoming increasingly relevant for India as copper demand is expected to rise sharply with expanding EV production and renewable energy installations. Any disruption in copper supply or increase in production costs could impact battery manufacturing economics and broader electrification initiatives.

India’s recent move into copper foil manufacturing, with investments from companies like Hindalco Industries, makes it even more important to have a steady supply of copper. Copper foil is a key material for anodes in lithium-ion batteries, and its success depends on reliable copper sources.

Implications for Cobalt Markets

Cobalt is less affected by sulphur risks because it is mostly made as a by-product of nickel and copper mining. Still, the report says that cobalt supply risks are tied to what happens in the nickel and copper industries.

India now depends on imported cobalt chemicals, but as the country builds more battery factories, changes in cobalt supply could affect cathode production.

Rare Earth Magnets and EV Motors: An Indirect Sulphur Connection

Sulphur market problems can also impact India’s fast-growing electric vehicle parts market. Permanent magnet synchronous motors (PMSMs), which are common in electric two-wheelers, cars, buses, and commercial vehicles, use high-performance neodymium-iron-boron (NdFeB) magnets.

Making rare earth elements like neodymium, praseodymium, dysprosium, and terbium involves a lot of acid leaching and solvent extraction, which use large amounts of sulphuric acid. Rare earth concentrates are often roasted with sulphuric acid before they are separated and purified.

China leads the world in refining rare earths and making magnets, supplying most of the global NdFeB magnets. If sulphuric acid prices go up, it could make refining more expensive and push up the prices of rare earth oxides and magnets.

This is a big concern for India. The country imports many of the rare earth magnets it needs for EV motors, industrial automation, and electronics. As more people buy EVs, higher magnet prices could raise the cost of making motors and affect the overall price of vehicles. This is especially important for PMSM-based electric vehicles, which are popular because they are efficient and powerful.

India’s EV Ambition

India has set up one of the most ambitious plans for EV and battery manufacturing in the world. Government programs like the ACC PLI Scheme, Auto PLI Scheme, PM E-Drive, and the National Critical Minerals Mission aim to build a strong local industry for battery cells, cathode materials, copper foil, EV parts, and recycling. But the recent problems in the sulphur market show that just having access to minerals is not enough.

Table1: Exposure of India’s Battery Ecosystem to Sulphur-Intensive Materials

| Material | Sulphur dependency | Indian exposure |

| Nickel (HPAL) | Very high | High |

| Lithium refining | Very high | High |

| Rare earth processing | High | Very high |

| High-Purity Manganese Sulphate Monohydrate (HPMSM) | High | High |

| Copper (SX-EW) | Moderate-high | Medium |

| Cobalt | Indirect | Medium |

Source: CES Analysis and Secondary Sources

India remains dependent on imported sulphur and sulphur-based chemicals. Domestic refining infrastructure for lithium, nickel, cobalt, and precursor materials is still at an early stage compared with global leaders like China, South Korea, and Japan.

As India builds more gigafactories and pushes for local production, the supply of sulphuric acid could become a major bottleneck. This could affect many areas at once, including battery materials, copper foil, rare earth magnets, and EV motors.

Strategic Opportunities for India

The country has identified significant lithium resources in Jammu and Kashmir and is actively acquiring critical mineral assets in countries such as Australia and Argentina to improve long-term raw material security. Recognizing the importance of developing domestic midstream capabilities, the Ministry of Mines is preparing a ₹3,000 crore incentive scheme to support lithium and nickel processing capacity in India, helping reduce dependence on imported refined materials and strengthen the domestic battery supply chain9.

However, securing mineral resources alone will not be sufficient. If India does not build adequate sulphuric acid production capacity, refining infrastructure, and integrated chemical processing capabilities, the cost of converting lithium and nickel into battery-grade materials will remain vulnerable to fluctuations in global sulphur markets. This exposure is particularly important because sulphuric acid is a critical input for lithium refining, nickel HPAL processing, and several downstream battery-material production routes.

Even with these challenges, the disruption in the global sulphur market also creates new opportunities for India. While the country has limited native sulphur resources compared with major producers in the Middle East and North America, growing demand for battery materials strengthens the case for expanding domestic sulphur recovery from refineries and petrochemical facilities, investing in sulphuric acid manufacturing, and developing integrated critical-mineral processing hubs. These priorities align closely with the National Critical Mineral Mission (NCMM), which seeks to build resilient domestic value chains for critical minerals through investments in exploration, overseas asset acquisition, processing, recycling, and technology development.

As India’s battery manufacturing sector expands, strategic priorities should extend beyond increasing sulphuric acid capacity. Policymakers and industry stakeholders should secure diversified sulphur supply agreements, enhance sulphur recovery from domestic refining and petrochemical operations, develop dedicated chemical parks for battery-material processing, and establish strategic reserves of sulphur and sulphuric acid. These actions would improve resilience to global supply shocks and support the growth of domestic lithium refining, nickel processing, precursor materials, and rare-earth value chains.

Recycling is another critical long-term solution. Recovering lithium, nickel, cobalt, and copper from end-of-life batteries requires significantly less primary mining and sulphur-intensive processing than producing these materials from virgin resources. India has already introduced a ₹1,500 crore incentive scheme for critical mineral recycling under the NCMM, highlighting the growing importance of circular supply chains in strengthening resource security, reducing import dependence, and supporting sustainability objectives10.

Conclusion

The recent jump in sulphur and sulphuric acid prices shows that supply chains for key minerals involve more than just lithium, nickel, and cobalt. Sulphur is now a crucial part of battery manufacturing, affecting the costs of refining lithium, processing nickel, making copper, and supplying cobalt.

For India, aiming to become a global leader in battery manufacturing, having a steady supply of sulphur and sulphuric acid is just as important as securing key minerals. Companies building gigafactories, making battery materials, producing copper foil, and recycling should make sulphur supply a part of their long-term plans. Countries that create strong and flexible chemical supply chains will be best placed to lead the next stage of the global battery industry.