In Part 1 of this series, we looked at the structural capacity gap forming across SPP’s 14 state footprint. The ISO’s capacity above peak load is projected to decline from 20.7% to negative by 2030, driven by 3,645 MW (summer)1 and 4,143 MW (winter)2 of coal and gas retirements and a new 36% winter Planning Reserve Margin (PRM), while rising deficiency penalties are reshaping the economics of capacity procurement. From Part 1, the conclusion was clear that SPP urgently needs new resources.

But understanding that SPP needs resources is only half the equation. The other half is understanding whether and how quickly these resources can actually interconnect to the grid. Between an attractive market signal and an operating battery project lies one of the most complex and consequential processes in the energy industry, the interconnection queue.

This part will provides a comprehensive guide to SPP’s interconnection process: the study mechanics, the queue data, the cost dynamics, and the strategic pathways that determine which battery projects actually get built. If you’re developing battery storage, evaluating project siting, or planning utility procurement, the interconnection queue is where your project either advances or dies.

SPP’s Generation Queue at a Glance: Around 150 GW and Growing

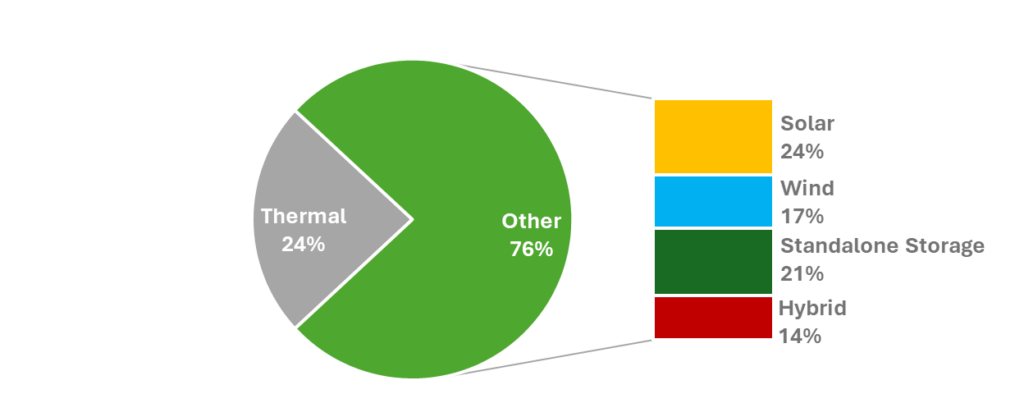

SPP’s generation interconnection (GI) queue currently has around 150 GW of total generation capacity,3 making it one of the largest in the country relative to installed system size. The queue has grown more than five-fold since 2013. Critically, the composition of the queue has shifted dramatically: renewables and storage now dominate, accounting for around 76% of queued capacity.

Solar and wind together make up nearly 41% of all queued capacity, with over 60 GW tentatively targeting commercial operations by 2031. With current install capacity of 423MW (as of Dec. 2025), standalone battery storage has surged past 31 GW in the queue. Hybrid queue capacity is around 20 GW and thermal projects, including natural gas, sit at around 35GW.

SPP IQ Tops ~150 GW, Up 5× Since 2013, with 76% RE & Storage

Active Queue Request | %

Source: CES, SPP

Figure 1: SPP Interconnection Queue (Feb 2026)

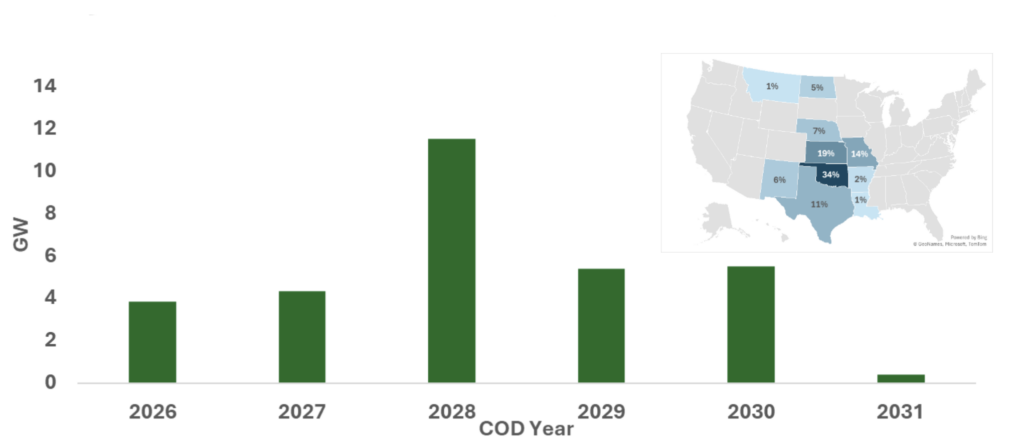

Standalone battery storage has gone from a footnote to a dominant force in SPP’s interconnection queue. In late 2017, SPP’s queue contained less than 1 GW of battery storage resources. Today, over 31 GW of BESS capacity is queued across SPP, making standalone storage the third-largest resource type in the pipeline after solar and thermal.

SPP Standalone Storage Jumps from <1 GW (2017) to >31 GW Today

SPP Standalone Storage Queue Outlook | GW

Source: CES, SPP

Figure 2: Standalone Storage Queue Outlook (Feb 2026)

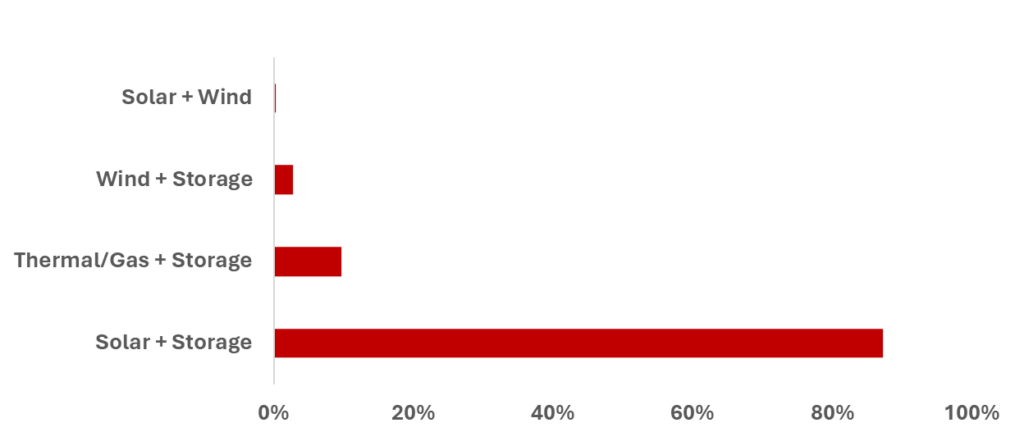

In hybrid projects, around 87% of the project storage is paired with solar, 10% are paired with thermal or gas, and approximately 3% are paired with wind. 4-hour duration storage dominates the queue, reflecting developers’ focus on maximizing resource adequacy accreditation value and evening peak load handling. This composition aligns directly with SPP’s ELCC structure, which awards up to 100% accreditation for four-hour systems at current penetration levels, as covered in Part1

87% of Hybrid Projects Pair Storage with Solar

SPP Hybrid Queue Composition | %

Source: CES, SPP

Figure 3: Queue Hybrid Composition (Feb 2026)

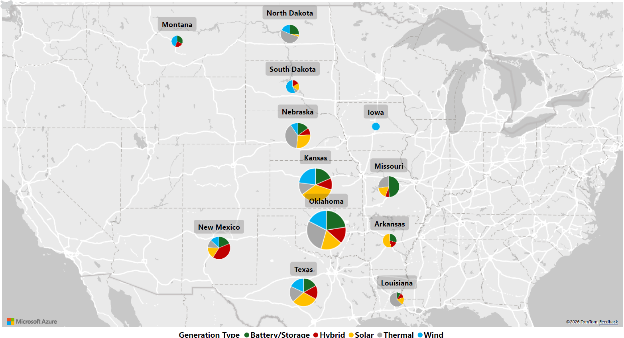

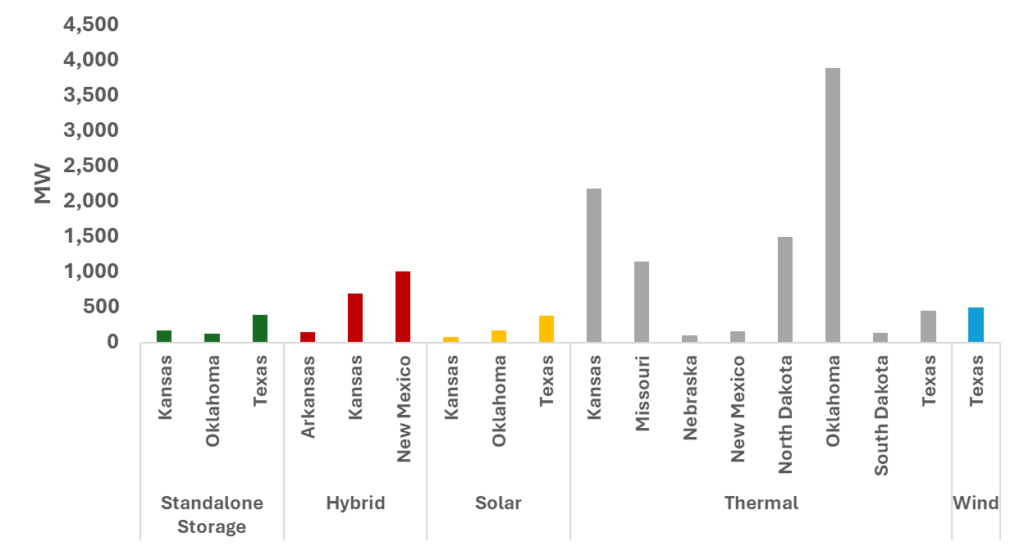

The southern and central parts of the region of SPP, notably Oklahoma, Kansas, Texas, and nearby states, have emerged as particularly active zones for queued projects. This trend is mainly driven by favorable grid access and development economics.

Source: CES, SPP

Figure 4: Location Composition (Feb 2026)

How SPP’s Generation Interconnection Process Worked

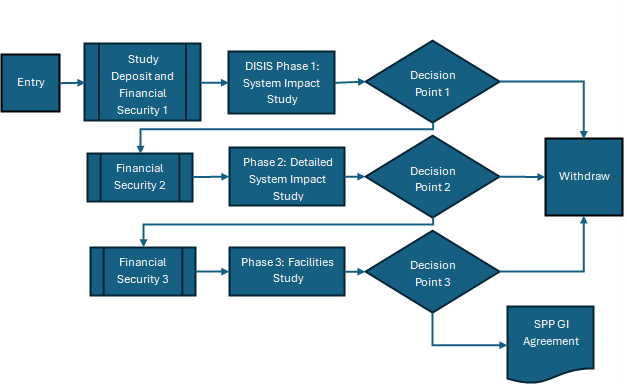

Governed by Attachment V of the Open Access Transmission Tariff (OATT), the Definitive Interconnection System Impact Study (DISIS)4 moved SPP from a serial approach to a three-phase cluster study.

- Study Window: Developers submitted requests during an annual 11month DISIS Quene Cluster Window.

- Three-Phase Evaluation: Requests were studied in three sequential phases, each followed by a Decision Point where developers had to provide additional financial security or withdraw.

- Phase 1 System Impact Study: SPP identified potential network upgrades required and provided preliminary cost estimates.

- Phase 2 Detailed System Impact Study: SPP updated network upgrade requirements and cost estimates after the withdrawals from Decision Point 1.

- Phase 3 Facilities Study: Final cost estimates to prepare for the Generator Interconnection Agreement (GIA) among the project owner, utility/transmission owner (TO)and SPP.

Source: CES, SPP

Figure 5: Three-Phase DISIS Flowchart

SPP recognized that the standard DISIS queue alone cannot move fast enough to meet the region’s emerging resource adequacy needs. As a result, SPP created twoaccelerated pathways.

Expedited Resource Adequacy Study (ERAS)

Approved by FERC in July 20255, ERAS created a one-time parallel interconnection study pathway that ran entirely separated from the standard DISIS queue. The process was only open to projects nominated by load responsible entities (LREs) facing resource adequacy challenges. The project qualifications worked as following:

Source: CES, SPP

Figure 6: ERAS Framework

As of Feb 2026, approximately 13 GW of capacity was under ERAS consideration. Thermal resources lead the ERAS race followed by hybrid projects. SPP estimates GIA execution will begin as early as possible in 2026.

Around 13 GW in ERAS Pipeline, Led by Thermal & Hybrids

SPP ERAS Resources Outlook | MW

Source: CES, SPP

Figure 7: ERAS Resources Outlook

Surplus Interconnection Service (SIS)

For battery developers looking at co-location, SPP’s SIS process enables faster approvals for hybrid and co-located projects that can utilize existing interconnection capacity. If an operating generator facility has unused capacity at its point of interconnection (POI), a storage project can apply to use that surplus capacity under a Surplus Interconnection Agreement (SIA) rather than a full GIA by going through the full DISIS queue, which is significant timeline advantage.

Next Big Update: Consolidated Planning Process

The Consolidated Planning Process is the most significant recent reform to SPP’s planning and interconnection framework. Approved unanimously by SPP’s Board of Directors in August, 2025,6 filed with FERC in November, 20257, and accepted by FERC on March 13, 20268, with an effective date of March 1, 2026, the CPP replaces two historically separate processes – the Integrated Transmission Planning (ITP) process and DISIS – with a single, integrated framework under a new Attachment AY of SPP’s Open Access Transmission Tariff.

The transition to the CPP represents a fundamental shift in how interconnection customers budget for grid access. Most importantly, it moves SPP away from the legacy DISIS approach of assigning network upgrade costs based on each project’s system impacts and replaces it with a more uniform and predictable Generation Resource Interconnection Deliverability Cost (GRID-C) structure. Under the prior framework, generator interconnection and transmission planning were conducted separately: ITP identified broader system transmission needs and allocated those costs to load, while DISIS studied individual generator requests and assigned upgrade costs to generators on a project-specific basis. This separation often resulted in duplicative engineering work, siloed cost allocation, and upgrade decisions that did not fully account for the combined needs of generation and load.

The CPP is intended to eliminate these silos by integrating transmission planning and generator interconnection into a single process. Rather than waiting for interconnection requests to arrive and then assessing upgrade needs on a case-by-case basis, SPP will proactively forecast transmission needs associated with both generation and load and develop a consolidated transmission portfolio to address them. The costs of that portfolio will then be allocated between generation and load based on the benefits each receives.

At the center of this new framework is GRID-C, the CPP’s centralized cost allocation mechanism for interconnection customers. GRID-C is a per-megawatt charge designed to recover the interconnection customer share of the CPP Transmission Portfolio costs. It replaces the legacy proportional impact method used under DISIS for assigning system network upgrade costs. Under the GRID-C framework, interconnection customers will no longer face highly project-specific upgrade assignments derived from individualized impact studies. Instead, they will pay a known, predetermined rate that will be published before the cluster window opens and will be based on the amount and type of requested interconnection service, such as ERIS or NRIS. In practical terms, this gives developers a more standardized and transparent entry fee for grid access and materially reduces the uncertainty associated with the prior DISIS process.

Transition from DISIS + ITP to CPP

With the March 1, 2026 effective date now confirmed, SPP expects the first CPP planning cycle to begin thereafter, with the initial study process concluding in 2028. The firstInterconnection Cluster Study (ICS) queue window will open 30 days after the effective date and close 60 days after SPP posts the initial GRID-C rate, which is expected by endof 2026.

The Next Disruption: When the Large Load Comes

Most of the developments discussed above – including the generation interconnection queue, ERAS, SIS and CPP – have largely been shaped from a generation-side perspective -. A new wave of demand from large load interconnection requests, driven by data centers, AI facilities, and broader industrial electrification, is poised to become the next major source of disruption in SPP.

In Part 3 of this series, CES will examine large load interconnection in SPP in greater detail, including High Impact Large Load Generation Assessment (HILLGA), Conditional High Impact Large Load Service (CHILLS) and Price Adaptive Load (PAL) processes. The discussion will also explore where the load growth is concentrating and how it may reshape nodal wholesale revenue for battery storage.

– Ann Yu & Shivam Chauhan